The 0.01% Trap: Why Your Savings Account Needs a System Upgrade 📉

We spend a lot of time on this blog talking about the mechanics of the stock market. We focus on maximizing TFSAs, understanding RRSPs, and buying broad-market ETFs. But before you can invest, you need a safe place to park your emergency fund and short-term cash.

For most people, that place is a savings account at the same traditional bank they have used since they were teenagers. The problem is that loyalty is costing you money. If your cash is sitting in a legacy bank earning 0.01% interest, it isn’t just sitting still. It is actively losing purchasing power to inflation.

It is time for a system upgrade.

The Legacy Code: Traditional Banks 🏦

Big, brick-and-mortar institutions are the legacy code of the financial world. When building my own financial stack, I have relied on traditional institutions like TD or RBC for certain day-to-day operations. They are excellent for specific use cases. For example, you might need a physical branch to get a bank draft, secure a complex mortgage, or deposit physical cash. But traditional banks carry massive overhead. They have to pay for prime real estate, physical security, and thousands of tellers. To subsidize those costs, they pay you practically nothing to hold your cash. Meanwhile, they lend that exact same cash out for mortgages and loans at 5% to 8%.

The Optimization: Fintech and High-Yield Savings 💸

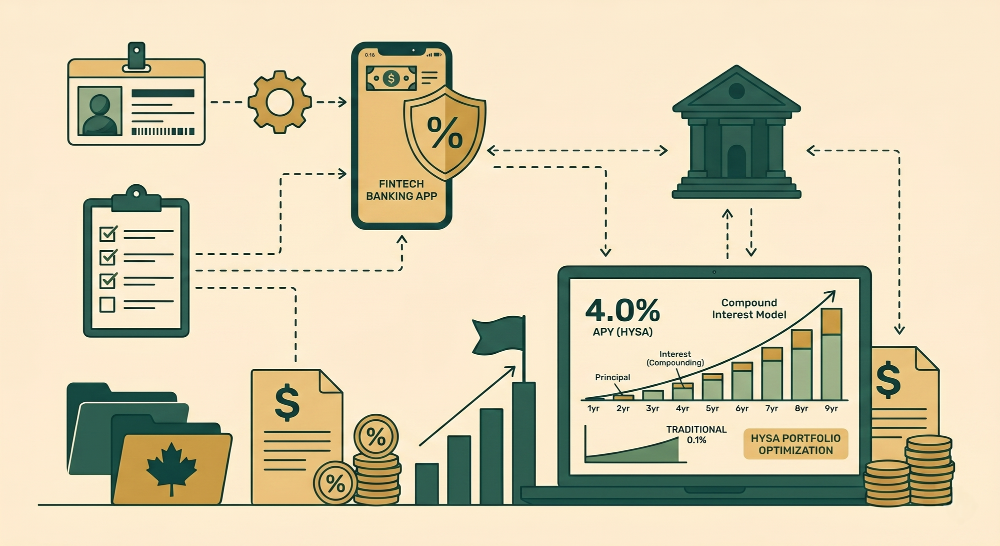

Financial Technology (Fintech) companies and online banks operate on a completely different architecture. They have stripped away the physical branches and the bloated legacy infrastructure. Because their operating costs are a fraction of the big banks, they pass the savings directly back to the consumer in the form of High-Yield Savings Accounts (HYSAs). Instead of earning pennies, these platforms routinely offer 4% to 5% interest on your idle cash. It is the exact same cash, parked in a mathematically smarter system.

But is it safe? 🔐

This is the most common roadblock. People trust the marble columns of a big bank. However, the top-tier Fintechs and online banks are heavily regulated. In Canada, accounts at institutions like EQ Bank or Wealthsimple are covered by the CDIC (Canada Deposit Insurance Corporation). This means your eligible deposits are insured up to $100,000 per category, exactly like the big banks. For my US readers, the equivalent is FDIC insurance.

The "Hub and Spoke" Banking System 📈

You do not need to completely abandon your traditional bank to take advantage of this. The most disciplined approach is a "Hub and Spoke" model: The Hub (Traditional Bank): Keep your Scotiabank, TD, or local bank checking account. Use this for your payroll deposits, paying your monthly utility bills, and e-transfers. Keep only enough cash here to cover 1 to 2 months of living expenses. The Spoke (Fintech HYSA): I actively route my emergency and idle cash into platforms like EQ Bank and Wealthsimple. This money sits slightly out of sight, earning a massive premium over traditional bank accounts and quietly compounding every month. I have personally transitioned away from banks to fintech for all day-to-day operations.

Start Optimizing Your Cash 🚀

If you are ready to upgrade your financial system and stop leaving money on the table, it takes about ten minutes to open an account online. Below are the tools I personally use to optimize my cash flow. If you use the referral links below, we both get a small cash bonus to kickstart the compounding process:

Wealthsimple Cash (🇨🇦) My go-to for an all-in-one financial ecosystem. Their Chequing account functions like a checking account but pays a high-yield interest rate, and it syncs perfectly with their investment platforms. 👉 Wealthsimple Referral Link

EQ Bank (🇨🇦) One of the pioneers of the high-yield space in Canada. No physical branches, no monthly fees, and consistently some of the highest base interest rates in the country. 👉 EQ Bank Referral Link

For my US readers, look into platforms like Ally Bank or SoFi for equivalent high-yield, no-fee structures.

Wealth is not just about making good stock picks. It is about optimizing every dollar in your system. Upgrade your savings today.