The Math of Consistency: Why Dollar-Cost Averaging Beats Market Timing ⏱️

Waiting for a stock market crash to buy at the bottom sounds strategic, but it is actually a wealth-killing trap. Here is why trying to time the market fails, and the mathematical system you should use instead.

The question I hear most often from beginners is always the same. They look at the stock market, see it hitting all-time highs, and ask if right now is a bad time to invest. They want to hold their cash on the sidelines and wait for a crash so they can buy at the bottom.

This sounds like a smart, strategic move. In reality, it is one of the most destructive financial habits you can build.

Trying to time the market requires you to be right twice. You have to perfectly predict when the market has hit its absolute bottom to buy in, and you have to know exactly when it has hit its peak to sell. Professional hedge fund managers fail to do this consistently. As retail investors, our chances are zero.

The solution is not to predict the market. The solution is to automate your behaviour.

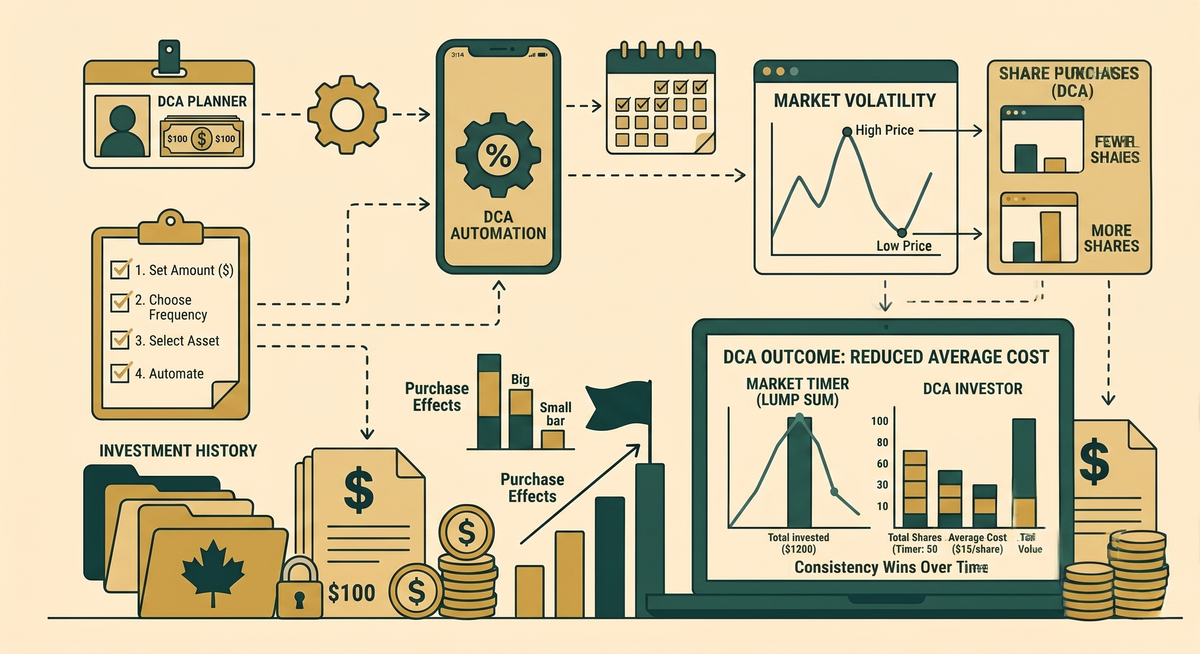

Enter Dollar-Cost Averaging (DCA) 💸

Dollar-Cost Averaging is a strategy where you invest a fixed amount of money at regular intervals, completely ignoring the current price of the market.

Instead of saving up $12,000 to invest all at once, you invest $1,000 on the first day of every month.

This creates a brilliant mathematical advantage. When the market is booming and prices are high, your fixed $1,000 buys fewer shares. When the market inevitably crashes and prices drop, that exact same $1,000 automatically buys more shares on sale.

You naturally buy more when prices are low and less when prices are high, without ever having to look at a chart or make an emotional decision.

Removing the Human Element 🤖

The greatest threat to your wealth is not a stock market crash. The greatest threat is your own psychology.

When the market drops 20%, human nature screams at you to hoard your cash and stop investing. DCA takes that decision out of your hands. It turns investing into a cold, calculated utility bill that gets paid every two weeks.

This philosophy of removing human error is exactly why I am developing Vivid, my personal finance coaching application. We cannot rely on motivation to build wealth because motivation fades. We have to rely on systems. A good financial tool should help you build an automated framework that executes your strategy in the background while you focus on living your life.

How to Build the System Today 🏗️

Setting this up takes less than fifteen minutes.

- Pick your number: Decide on a realistic percentage of your paycheck that you can invest right now.

- Automate the transfer: Log into your checking account and set up a recurring transfer to your TFSA or RRSP on the exact day you get paid.

- Automate the purchase: Platforms like Wealthsimple allow you to auto-invest your cash into a broad-market index fund the moment it hits your account.

Stop checking the news. Stop looking at the charts. Build the machine and let the math do the heavy lifting.